Recent News

Hong Kong Property Market Forecast for 2026 More

2025-01-13

Hong Kong Property Market Forecast for 2025 More

2024-01-24

Hong Kong Property Market Forecasts for 2024 More

2023-03-02

[P Mortgages] What is a P mortgage? And is it the best choice for buying a property? Should I choose P, H, or fixed-rate mortgages when buying a property? More

2022-01-26

OneDay Vietnam Officially Launched More

2021-11-15

Vietnam Land For Sale | Rare Seafront plot in Da Nang 40+ Acres More

2020-11-03

Estate Agent App 2.0 Launched More

2020-09-28

Top Tips On Buying Hong Kong Industrial Property | OneDay More

2020-09-15

Car Park Investment 2020 More

2020-09-05

Eligibility for SME Financing Guarantee Program More

9 Steps to Purchasing Property in Hong Kong with Mortgage

2018-09-04 | Author:

Hong Kong is one of the easiest places to purchase properties; the procedures are simple and you can either purchase the property with your own name or your company's name or jointly with your partner. This 9 step guide is for those who want to purchase a property in Hong Kong with financing on the second-hand property market.

1. Get a Mortgage Pre-Approval

A lot of people will purchase a property in Hong Kong with a mortgage and it is generally sensible to speak to a bank before you make an offer on a property so that they can assess how much they can lend to you for the property purchase based on your financial situation. Most banks will ask you for your bank statements for the last 6 months, tax return, MPF payment records, etc. so that they can calculate how much they can lend to you from which you can work out a budget for your property purchase. As of writing, ie. 2018, the maximum that a bank will lend for a residential property that is under HK$ 10million is 70%; so for a property of HK$ 10million you would need to put down at least 30% as down payment. For commercial & industrial properties the banks can only lend a maximum of 30% of the total purchase price. For first-time residential property purchasers, it may be possible to borrow up to 90% of the property price provided that the property is under a certain amount but certain conditions apply.

2. Search for, Vet and Identify the Property

Online is a good place to search for properties because you can do it anytime, after work, before work, whilst you are travelling or just waiting around. There are some great sites that list properties for sale - some belong to estate agents and are run independently. Sites include OneDay (https://www.oneday.com.hk), Net Property (http://www.netpropertyco.com), Q Fang (http://hk.qfang.com). Most of the properties for sale are marketed by estate agents and it would be wise to go through an estate agent for your property purchase as they can help you throughout the entire purchase process, from doing the background ownership check on the property to negotiating a good price. Typically the estate agent will charge 1% commission of the purchase price which you pay upon completion of the entire deal. The commission may vary from agent to agent and property to property but is typically 1%. It is probably worth viewing a number of properties that you wish to buy so that you can see where the market is at and unless you know exactly where you wish to purchase then it may be worthwhile seeing some properties in a few different districts just to get a feel for the market. After viewing a number of properties and you have identified the property you wish to purchase then it you can make an offer on the property.

3. Agree on a Price with the Seller

The estate agent will help you to put in an offer to the seller and the role of the estate agent in the price negotiation can be quite useful as the estate agents are more effective at getting a better price than if you would do the negotiations directly with the seller. Once you and the seller agree on the price then the next part will be to draw up the Preliminary Sale & Purchase (S&P) Agreement.

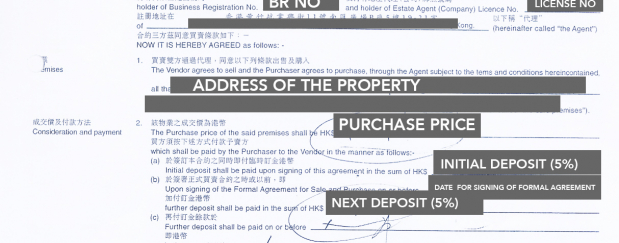

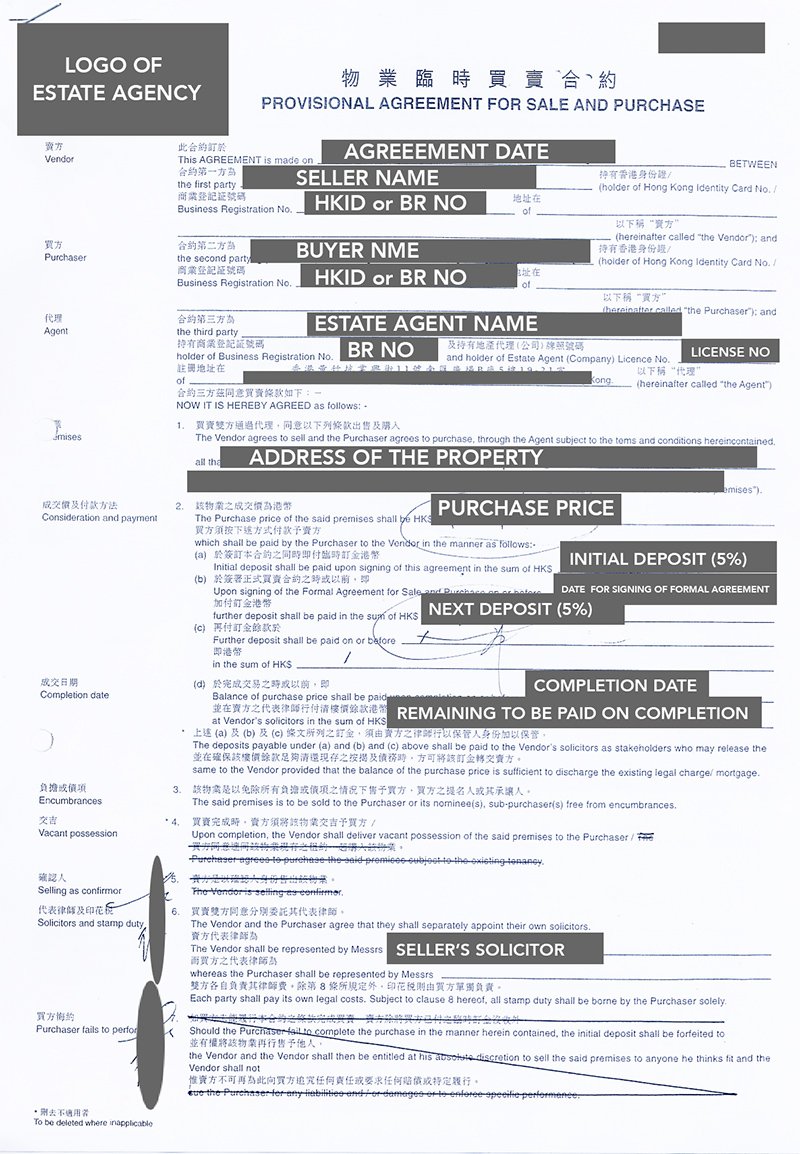

4. Enter into a Preliminary Sales & Purchase Agreement and Pay Deposit

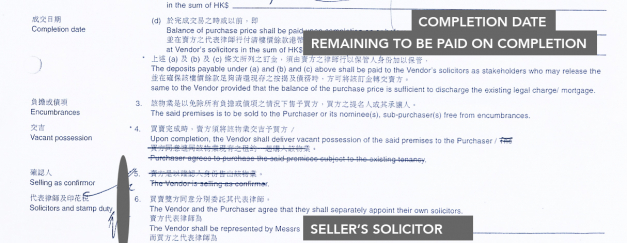

In terms of timing; most of the time the completion date (the date when the entire deal is done and the property's ownership is transferred to you) is set to 2 months from the date of the signing of the preliminary S&P Agreement; the setting of the completion date is completely open and is up to the seller and the purchaser to agree upon. However usually, it is rarely set to a date more than 6 months from the signing of the Preliminary S&P agreement. The other key cornerstone to this agreement is that both parties need to set a date for the signing of the formal Sales & Purchase agreement which is usually set at 14 days after the signing of the Preliminary S&P agreement along with the payment of another 5% of the total purchase price. The Preliminary S&P agreement is usually a simple 2-pager with key details of the purchase such as the purchaser, the seller, the property details, agreed price, date when both parties will enter into the formal sales & purchase agreement, completion date and other terms such as whether the property would be delivered in vacant possession or whether tenanted. Typically 5% of the total purchase price will be payable to the seller upon execution of this agreement which is the initial deposit. If for whatever reason you decide not to go through with the purchase then you will most likely forfeit this deposit. Whereas if the seller decides not to go through with the sale then they will have to pay you back the 5% deposit and an additional 5% as penalty. These are the typical terms for purchasing second hand property but for first hand property transctions where the seller is a big property developer then the terms may be different. Once you have the Preliminary S&P agreement, send a copy to the bank so that they can start the mortgage application process immediately; this can take a few weeks so get this part done immediately The below is a sample preliminary sales and purchase for a commercial property purchase.

5. Enter into a Formal Sales & Purchase Agreement

As soon as the Preliminary S&P agreement is signed then you will need to have a solicitor or lawyer in place who will help to draft the final version of formal S&P agreement. Sometimes buyers will assign a solicitor before entering into the preliminary S&P agreement. The vendor's lawyer will normally come up with the first draft of the formal S&P agreement which they would send directly to your lawyer for review. Most of the terms of the formal S&P agreement will be based on those in the preliminary S&P but in more detail. The formal S&P agreement is normally signed by both parties 14 days after the signing of the preliminary S&P agreement and you will need to pay another 5% of the total purchase price to the seller. Normally all of the monetary transactions will go through the lawyer who will deliver the signed agreement along with transferring the money to the seller's lawyer; so your lawyer would usually ask you to send through the other 5% deposit of the purchase price a few days before the exchange of the formal S&P agreement so that there is ample time for cheques or funds to clear. You will also need to go to the lawyer's office to sign the formal S&P agreement either on the day it is supposed to be exchanged or a day or so before. Once the formal S&P agreement has been signed; it will be very difficult to turn back.

6. Sign Mortgage Documents

The reason why most deals are set to 2 months from the date of signing is so that it gives the buyer sufficient time to arrange mortgage facilities with banks. For transactions whereby the buyer pays with cash for the purchase sometimes the deal window is set to 1 month or even shorter. Even with mortgage pre-approval, it can still take the banks a few weeks to process your mortgage application and you may need to give them updated statements and/or other information. Usually the banks would do a valuation of the property first and they would lend you a percentage of either the property sales price or their valuation (whichever is lower); banks vary slightly on their valuation and mortgage terms so some people will shop around to find the best deal. Usually after about a month from the time you send to the banks the preliminary S&P documents they will have approved the mortgage and you will need to go to the bank to sign the relevant documents. On completion date, the banks will send the money directly to your lawyer who will then send the money to the seller; so the lawyer will usually handle all of the money-side of the transaction and you do not need to worry about this part.

7. Do a Final Property Inspection

This often seems like a superfluous step because all of the paperwork is already done and it would be hard for either party to back down. This step is usually conducted around 2 weeks before completion date; the buyer will be allowed to do a final property inspection to make sure that the property still exists and that there are not any major structural problems with it that have emerged since the time the Preliminary S&P agreement was signed. This step is more a formality and I must admit I have never been in a situation where the buyer has raised a serious issue and threatened to withdraw from the deal ensuing a final property inspection.

8. Sign All Documents at the Lawyer's Office and Pay All Remaining Amounts & Fees

A few days before the completion date, you will need to send to your solicitor or lawyer all remaining amounts for the property purchase and you would be required to sign a number of other documents to do with the mortgage, insurance, deed transfer, etc. So far, you would have likely paid 10% of the purchase price and if the bank provides a 70% mortgage for the purchase then the remaining 20% of the purchase price would need to be paid to the lawyer. Quite often, at this juncture you will pay the agency fees, stamp duty, legal fees, electricity transfer fees, etc. The legal fees are usually charged at a flat rate of around HK$ 10,000 depending on who you use. Once this step is complete, you can pretty much sit back and wait for the completion date because everything that you need to do will have been done.

9. Get the Keys to Your Property

On the completion date, if it was agreed that you will receive the property in vacant possession then by day end of the completion date your lawyer would have been given a set of keys for the property and you can pick up and enter your very own property.

Disclaimer This article is for reference only and does not constitute legal advice; buyers and sellers should make their own enquiries. We make no warranties explicit or implied on the accuracy and validity of the information given hereunder.